Housing Highlights from the 2014 American Community Survey

Published On September 16, 2015

The Census Bureau has just released the 2014 American Community Survey (ACS), the most detailed and comprehensive regular source of housing data for the U.S. and local areas. The data show a housing market that remains in recovery, with concerns about rental affordability alongside longer-term issues like declining homeownership. As always, underlying the national trends are huge differences among local markets. Here are the housing highlights from the 2014 ACS, with more detail available in this slide deck.

Homeownership and household formation:

- The homeownership rate fell to 63.1% in 2014 from 63.5% in 2013, down from a peak of 67.3% in 2006 (slide 4).

- Among large metros, the 2014 homeownership rate ranged from almost 70% in Minneapolis-St. Paul to just 48% in Los Angeles (slide 5).

- In 2014 compared with 2006, there were 3.9 million more single-family home renters and 2.7 million more apartment renters. However, between 2013 and 2014, the number of single-family home owners increased slightly, the first increase in four years (slides 6 and 9).

- Household formation was 968,000 in 2014 – higher than the recession-era average but still below the “normal” level of 1.2 million (slide 10).

Housing costs:

- The share of households spending 30% or more of their income on housing (“cost-burdened” households) fell to a post-bubble low of 34.6% in 2014, down slightly from 34.8% in 2013 and from a peak of 38.1% in 2010 (slide 12).

- Among large metros, the share of cost-burdened households in 2014 ranged from a high of 48.4% in Los Angeles and 47.0% in Miami to a low of 26.8% in Pittsburgh (slide 13).

- Nationally, 50.1% of renters in 2014 were cost-burdened, versus 31.2% of owners with a mortgage. The cost-burdened share among renters climbed during the recession and remains high. At the same time, refinancing activity and lower mortgage rates reduced the cost-burdened share of owners with mortgages significantly, from 38.3% in 2010 to 31.2% in 2014 (slide 14).

Vacant homes:

- The vacancy rate in 2014 remained unchanged from 2013, at 8.4% (excluding seasonal vacancies). Low household formation meant that vacant homes did not fill up, despite below-normal construction activity. The vacancy rate has fallen from a peak of 9.1% in 2010 but in 2014 was still slightly above its 2006 level (slide 16).

- Among large metros, the vacancy rate (excluding seasonal vacancies) ranged from over 12% in Birmingham, AL, to under 4% in San Jose (slide 17).

- Compared with the bubble years of 2005 and 2006, there were fewer vacant homes for sale or for rent in 2014. However, there were more vacant homes being held off the market or being used occasionally or seasonally. This shift toward vacancies that are not transacting is why active inventory is tight while overall vacancy rates are still elevated (slide 18).

- The vacancy rate for single-family homes was 10.7% in 2014, near its peak of 11.0% in 2011 and well above its 2006 level. In multi-unit buildings, however, the vacancy rate dropped to 14.9% in 2014 from a peak of 17.2% in 2010 (slides 19 and 20).

The full set of slides is available here.

A spreadsheet with selected data for the largest metros is available here.

Share This Post:

Related Articles

Student Capstone Projects

As part of our commitment to the education and professional development of UC Berkeley students, the Terner Center highlights exceptional…

Lessons from California’s Statewide Efforts to Affirmatively Further Fair Housing

To counter the impacts of decades of discriminatory housing policies and worsening racial segregation, the State of California established a number of Affirmatively Furthering Fair Housing (AFFH) strategies. Designed to foster racially and economically inclusive, opportunity-rich communities, these efforts were intended to facilitate effective local fair housing planning and enacting statewide policies to promote integrated communities. A new Terner Center policy brief highlights key AFFH strategies, noting areas of progress and where additional efforts are needed. It examines California’s successes and challenges since 2016, offering recommendations for other states working toward fair housing goals.

Addressing the Housing Needs of Low-Income Households in the Bay Area: The Importance of Public Funding

This policy brief explores how public funding can address the San Francisco Bay Area's housing affordability crisis by increasing the…

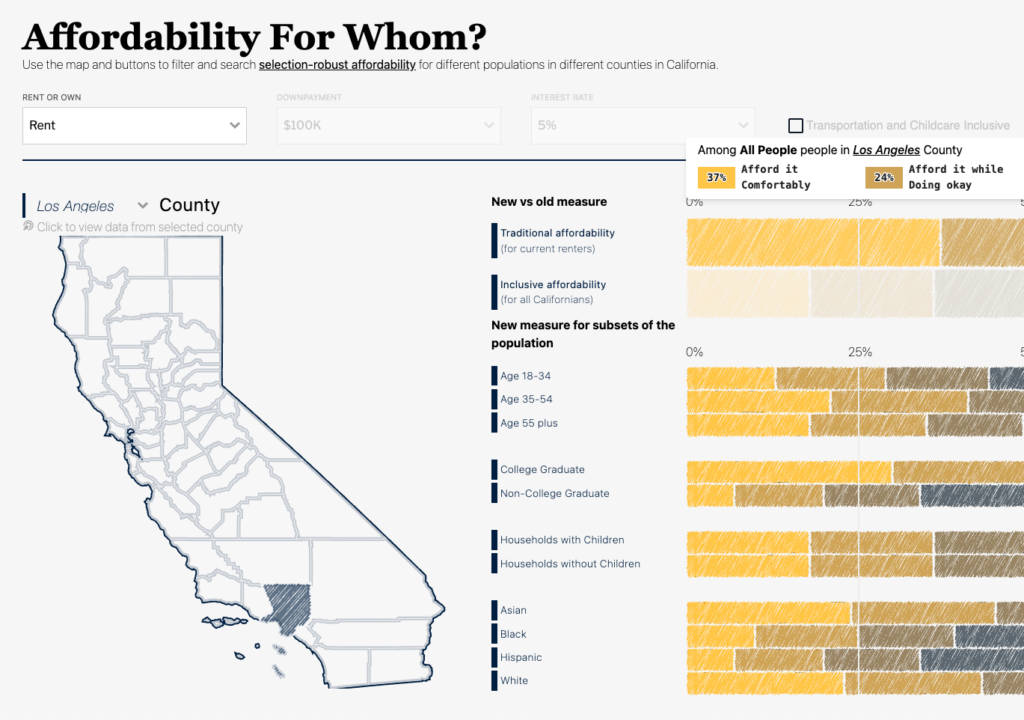

Affordability for Whom? Introducing an Inclusive Affordability Measure

This paper presents a new approach to measuring housing affordability—one that seeks to provide a better indicator of what counties…